The Complex Story of Britain’s Unpaid Wartime Debt to India:

A Burden Equal to 10% of India’s GDP in 1947

The financial legacy of British colonialism left India with enormous economic ruin at independence. One of the most glaring example was the massive wartime debt Britain owed India. This debt was so large that it amounted to roughly 10% of India’s entire economy in 1947, underscoring the profound injustice and long-term economic harm caused by Britain’s refusal to fully honor its obligations.

Yesterday PM Modi arrived in London for a two-day UK visit focused on signing a historic Free Trade Agreement and strengthening the India-UK Strategic Partnership. He is also scheduled to meet PM Keir Starmer and King Charles III during this trip.However UK had been not only brutal coloniser of India but was also dishonest in its dealings with India, after Britain had left India. It refused to honour it’s obligations towards India.

The Great British Heist?

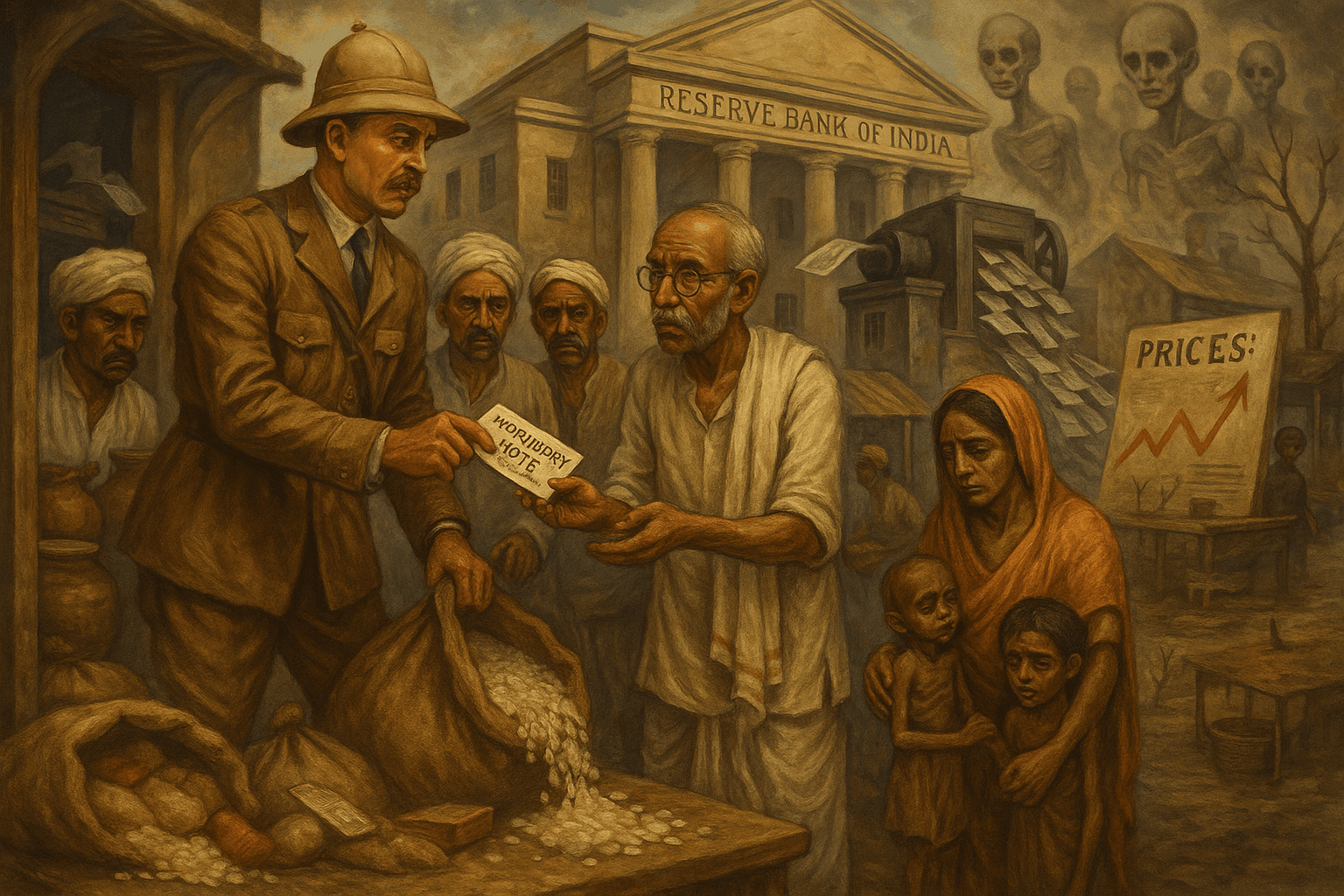

The resources that Britain obtained from a poor India during WW-2 were comparable or exceeded that provided by an increasingly prosperous United States. While American materials were provided after Britain signed an agreement on Washington’s terms, the Indian story was rather different. Britain coveted India’s resources but did not want to pay for them. As a result, in lieu of payments for goods and services drawn out of India, Britain held promissory notes that were to be redeemed in the future. This is akin to a customer walking into a grocery store and clearing out the shelves. But instead of paying cash, he writes out a note promising to pay up later. Moreover, he decides to keep this note with himself for safe custody!

But if Britain deferred payments, the goods had to nevertheless be purchased in India against a cash payment to individual sellers. It is here that the Reserve Bank of India stepped in to the aid of London and printed a large amount of currency. Thus, between 1940 and 1942, the amount of money in circulation in India more than doubled. The result was an average rate of inflation of a whopping 350%. Rapid and sustained economic inflation is a most regressive form of hidden taxation as it severely and disproportionately penalizes the poor. Such inflation coupled with all-round scarcity of goods had a devastating effect on life in India. While the millions of deaths in the Bengal Famine of 1943 was a grim consequence of British policy in India, it was only the grisly tip of a vast iceberg of countrywide sorrow and hardship. (See link to wire.in below)

India’s Economy and Wealth at Independence

In 1947, India’s Gross Domestic Product (GDP) stood at approximately ₹2,700 billion (2.7 trillion rupees) — roughly equivalent to $20 billion USD at historic exchange rates, with a population of around 350 million, and a per capita income near $58 USD. India was among the world’s poorer economies at independence, burdened by widespread poverty, partition-related dislocation, and underdevelopment.

This scale is critical for understanding the magnitude of Britain’s wartime debt to India. The British government owed India about £1.16 billion sterling in accumulated sterling balances — India’s share of payments for its enormous contributions of troops, war supplies, and blocked export earnings during World War II. At the 1947 exchange rate (~₹13.33 per £1), this debt translated to approximately ₹15.5 billion.

Debt Equal to a Tenth of India’s Economy

Viewed in relation to India’s total GDP, the wartime debt Britain owed represented roughly 10% of India’s entire economic output at independence. For context, this is an exceptionally large sum, especially for a newly sovereign and economically fragile nation needing every rupee to fund reconstruction, relief, and development. India’s debt by 1945 was about £1.51 billion – the equivalent of $83.93 billion today.

Britain’s Strategy: Delay, Partial Payments, and Diplomatic Subterfuge

Despite this enormous liability, Britain did not fully repay India. Instead, the UK government pursued a careful and prolonged strategy to evade full payment:

- During the war, in 1939 itself, Britain suspended sterling convertibility, creating “blocked sterling balances” that grew to £3.35 billion, of which India’s share was about 45% (~£1.51 billion initially).

- As independence approached, Britain and the United States coordinated secretly to limit repayments to India, fearing that full repayment would cripple Britain’s postwar recovery and geopolitical role in the emerging Cold War.

- Sterling convertibility was briefly restored in July 1947 but suspended again a month later—on August 20, 1947—just before Indian independence, effectively blocking India’s access to much of its wartime funds.

- Britain agreed only to small initial payments (£35 million in 1947), with the bulk of the debt intended to be repaid over many years and sizable portions written off as “adjustments” or offset against counterclaims.

- India, starved of these funds, had to fund its wartime costs and reconstruction internally, resorting to heavy taxation and printing money, which caused inflation and economic hardship.

Economic and Political Consequences for India

The British strategy to postpone and minimize repayments was not a formal default but a de facto repudiation by bureaucratic and diplomatic delay. India suffered serious economic constraints as a result, at a time when the country urgently needed capital for rebuilding and development.

This prolonged financial subterfuge reflects the power imbalances of the colonial and early postcolonial era, where Britain leveraged Cold War geopolitics and economic weakness to evade its rightful obligations. The episode remains a stark example of how postcolonial financial justice was often sacrificed on the altar of geopolitical expediency.

Table: Economic Context and Debt Scale

| Metric | Approximate Figure (1947) |

|---|---|

| India’s GDP | ₹2,700 billion (≈ $20 billion USD) |

| India’s Population | ~350 million |

| India’s Per Capita GDP | ~$58 USD |

| British War Debt to India | £1.16 billion (~₹15.5 billion) |

| Debt as % of India’s GDP | Approximately 10% |

Summary:

The wartime debt Britain owed India was a colossal sum, equivalent to about a tenth of India’s entire economy at independence. Rather than repaying this fairly and promptly, Britain protracted negotiations, manipulated currency policies, and coordinated with the US to delay repayments and paid tiny sums in installments to keep the facade of payment. India bore the economic burdens imposed by this financial injustice during its critical formative years.

This episode exposes the harsh realities of economic inequality embedded within decolonization, illustrating how geopolitical and economic power enabled Britain to evade critical fiscal responsibilities while India grappled with poverty, inflation, and developmental challenges. It was a day time robbery for which UK has no explanation even today. Would Prime Minister Modi raise this issue on this visit to UK? I doubt it.

From 1947 to 2025: Economic Journey of India

References:

- Detailed analysis from The Wire on the UK-US diplomatic negotiations over sterling balances

- The Wire on: Britain’s debt to India, a complex story.

- Historical economic data on India’s GDP and sterling debt from credible economic sources and Bank of England records

- Research on India’s post-independence economic trajectory and British wartime economic policies