(Part 4)

Ease of Doing Business in India

How difficult is it to do business in India?

In Part 3 of this series, I had mentioned that in Dubai the Ruler’s word from his mouth becomes law. When a regulation is announced, it is implemented. When an official disobeys, consequences follow. In some cases, that official lands in prison.

In India, the law is dispensable. Discretion is mandatory in everything.

This is not about one sector or one ministry. Whether you deal with banks, GST departments, Income Tax offices, or Municipal corporations, the pattern repeats. Regulations are announced with fanfare. Prime Ministers and Finance Ministers speak about ease of living and ease of doing business. Nothing changes on the ground.

Discretion has made officers more powerful than the Ruler himself.

The Banking Example

Let me start with banking because everyone needs a bank account. The business starts with opening of bank account. The patterns of problems in opening a bank account apply everywhere else.

The Regulatory Law:

The Reserve Bank of India has simplified KYC (Know Your Customer) rules. According to RBI directives, banks must accept documents from DigiLocker, the government’s official digital document repository. For minor changes like email or phone number updates, banks should not ask for document resubmission if your identity is already verified.

The law is clear. The implementation is chaos.

Example: Three Bank Stories

Private Bank: The Disappearing Email

I needed to change my email address at a private bank. In October 2025, they asked me to open their app and guided me through the settings. There was OTP verification. Done.

It worked from November 2025 to January 2026. I received my account statements at the new email address. Then suddenly in February 2026, the statement landed in my old email.

I went to the branch. They are working on it. They do not know why it happened. In their records, the new email is reflected. They do not know why or how the statement was sent to the old email.

For the same bank, I needed to update KYC for my credit cards. Now they required Aadhaar. The Branch Manager called the dealing department. They said PAN would work, but it must be a xerox of the physical PAN card with a photograph. Alternately, a copy of Aadhaar would do.

Here is the problem. The Government of India provides these documents in its DigiLocker app. RBI has stipulated that banks must accept them. They don’t.

This particular bank manager used my Aadhaar card number to download a fresh copy on his laptop. I supplied him the OTP. Think about this carefully. A bank manager asked me to share an OTP. This violates every security protocol that banks themselves advertise in their campaigns. Yet he had no other way to comply with his own bank’s requirements.

He took a printout. He attached it to the KYC form. He affixed his signature mentioning that he downloaded and verified it personally. It had to be duly verified and self attested with my signatures too. He assured me he would send it to the Credit Card head office in Chennai. He also redacted all Aadhaar digits except the last four for privacy.

Let us hope it gets processed.

Another Private Bank: The Vanishing Request

Another bank wanted me to personally visit and fill a form to change my email address. I tried sending repeated emails. No response. Their app has no option for this change.

I complied. I gave them a signed form about three months ago. Nothing has happened so far. I will close this account soon.

Public Sector Bank disrespects Privacy

The third example is a public sector bank. I transferred my account from one branch to another. Both branches are located exactly 1,000 steps away from each other. The transfer happened in one day.

But changing KYC details like telephone number and email became a real problem. They insisted on full Aadhaar with all digits of number visible. They did not volunteer to download it themselves from DigiLocker. I gave them a copy with the full Aadhaar number as they insisted. It had to be duly verified and self attested with signatures.

It can be misused. But what choice did I have?

Opening Business Accounts

For a savings bank account, the procedure is relatively simple. You face the usual confusion between digital copies and physical copies as required for KYC.

But if you have a proprietorship firm or a Corporation Sole, you are in serious trouble. Some banks are satisfied with Udyam registration. Others insist on GST registration.

Now GST registration requires a turnover of Rs. 40 lakhs or more in most cases. So how will a micro or small business open an account if their turnover is below this threshold?

The answer is simple: it is the Manager’s discretion. They do not trust someone walking in without a reference.

The Exception

There are some institutions in India who have figured this out.

DBS Bank (Singapore’s digital bank operating in India) is an all-service bank with no physical branch requirement. Everything is online. They fetch information automatically from the Aadhaar website. Change your email or phone number with a simple OTP. No questions asked. No branch visits. No physical documents. They started working like this in 2018-19 itself.

Zerodha Kite, the online trading platform, follows the same model. Perhaps they require a PDF upload of the signature. Everything else is fetched automatically from Aadhaar. Changes happen with OTP verification. Change email, bank account or even phone number. No physical document required.

If they can do it, everyone can do it.

This is the critical point. The problem is not technical. The technology exists. The infrastructure exists. The Aadhaar system provides the backbone for digital verification. DigiLocker provides authenticated documents.

The problem is the institutional choice.

DBS Bank and Zerodha chose to follow the regulations as written. They chose to trust the digital infrastructure the government built. They chose to eliminate discretion by automating processes.

Traditional banks chose differently. They chose to maintain physical processes. They chose to give branch managers discretion. They chose to ignore digital documents despite RBI mandates.

Why? Because discretion gives power to officers. It creates dependencies. It maintains the old order where connections matter more than compliance. It preserves the colonial mistrust of ‘natives’.

The Universal Pattern

This is not unique to banking. The same pattern appears across every government interface.

GST Department: The law says one thing. The officer interprets it differently. Getting GST registration in 8 days is only a myth in which Minister of Finance can believe. Chartered Accounted are asking for ‘convenience fee’ to expedite. Two businesses with identical situations get different treatments depending on which officer handles their case. Appeals take years. Penalties are imposed first, justice comes later if at all.

Income Tax Office: Rules are clear on paper. But which documents are accepted, which deductions are allowed, which explanations are satisfactory depends entirely on the assessing officer’s discretion. The same return can be accepted in one zone and questioned in another. Worse is the website. Online return started at least 15 years ago. It still try to emulate the old paper form. Very difficult to navigate.

Municipal Licenses: Getting a trade license or building permission is not about meeting requirements. It is about which clerk processes your file, which officer signs it, and whether you know someone who knows someone. The same application can take two weeks or two years. Online application has options like chicken and egg and both are demanded together. For example when you ask for Trade License, it will ask for Commercial License first. But when you apply for Commercial License it will ask for Trade License. How can you have apply for one without the other is not clear.

Commercial Regulations: Every new business regulation is announced as a reform to improve ease of doing business. On the ground, it creates one more checkpoint where an officer exercises discretion. One more place where rules bend according to relationships rather than compliance. Try Trademark office or Transport Office. They have online presence but you need somebody to navigate through it.

How can there be ease of doing business if web sites are so difficult to use? There is no audit of websites for ease of use. There is no mail address of webmaster given on any website. A working or functional site is optional. Some day it may refuse to work.

Why Discretion Persists

First, no consequences for non-compliance. When a bank manager rejects a valid DigiLocker document despite RBI mandates, nothing happens to him. When a GST officer interprets rules creatively, no audit questions it. When a municipal clerk delays a file, no supervisor intervenes.

Second, lack of standardization. There is no common training, no uniform interpretation, no shared understanding of what regulations actually mean. Each office becomes its own kingdom with its own rules. In fact a branch manager will tell you that in that branch we ued to do like this but here the practice is this. This is an acceptable norm.

Third, the system rewards discretion. An officer who follows rules strictly is seen as difficult. An officer who exercises “flexibility” is seen as helpful. But flexibility means different rules for different people. It means connections matter more than compliance.

Fourth, appeals are costly and slow. Fighting an arbitrary decision takes more time and money than accepting it. Most businesses accept. The system continues.

Fifth, institutional resistance to automation. Automation eliminates discretion. When processes become digital and rule-based, officers lose power.

The Real Cost

These examples are from the most citizen friendly institutions that is banks. There are worst departments who exist only for bribes. It is impossible to get things done without paying the middleman.

This is not about inconvenience. This is about the fundamental nature of governance. In a rule-based system, you know what to expect. You prepare documents, meet requirements, get approvals. Success depends on compliance.

In a discretion-based system, you never know what to expect. One day is to visit a particular office for enquiry of exactly what documents are requied. Next day citizen comply with rules. Requirements sometimes change based on who is sitting across the desk. Success depends on relationships, references, and luck.

Small businesses suffer most. They lack connections to bypass arbitrary requirements. They lack resources to keep fighting. They often come up their own ingenious ways to bend the rules.

India ranks poorly in ease of doing business not because we lack regulations. We have plenty of regulations. We rank poorly because regulations are not rules. They are starting points for negotiation.

The Announcement vs Reality Gap

The Prime Minister announces initiatives. The Finance Minister speaks about ease of living. Digital India is promoted. Faceless assessments are introduced. Single window clearances are promised. Parliament passes laws. Ministries issue guidelines. But at the point of implementation, the officer decides.

None of it changes the fundamental reality. At every interface between citizen and state, discretion trumps rules. At the branch, at the office, at the counter, the officer still decides. The rule is still optional. The procedure is still whatever that particular person says it is.

That clerk who sits at the municipal counter has more power over your business than any policy announcement. That GST inspector who visits your premises has more impact on your operations than any budget speech. Recently they ask for a photograph of premises instead of insisting a visit but photo shoot itself is matter of debate. It can be rejected many times.

That bank manager who rejects your documents controls your access to finance more than any RBI circular. Discretion has made these officers more powerful than the Ruler. They cannot be questioned. They cannot be bypassed. They face no consequences for arbitrariness.

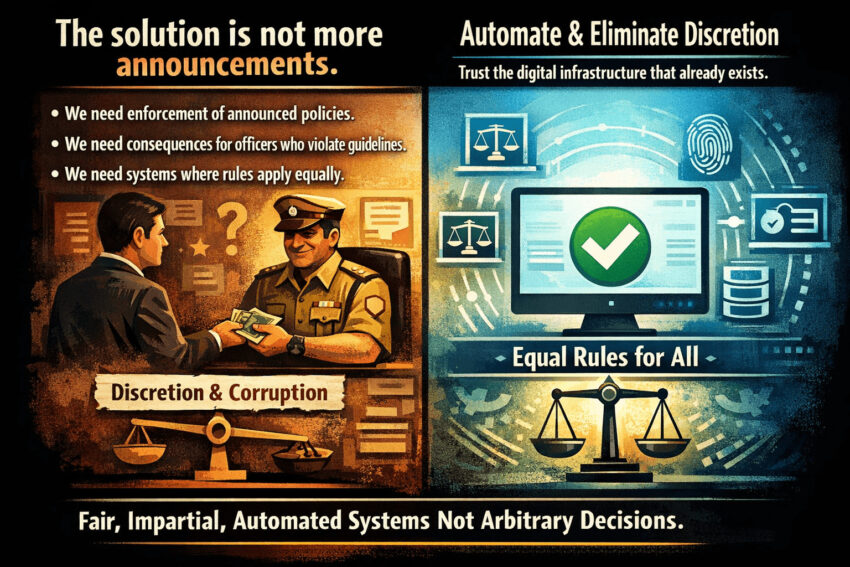

The Solution

The solution is not more announcements. We need enforcement of announced policies. We need consequences for officers who violate guidelines. We need systems where rules apply equally regardless of who processes your case.

DBS Bank and Zerodha show the path forward. Automate processes and eliminate discretion. Trust the digital infrastructure that already exists.

Most importantly, we need to recognize that discretion is not flexibility. Discretion is arbitrary power. And arbitrary power is the opposite of rule of law. Until discretion becomes the exception rather than the rule, doing business in India will remain an exercise in navigating personalities rather than following processes.

The craft of doing business in India is not understanding regulations. It is understanding that regulations are merely suggestions that each officer interprets as they please.

Reference:

RBI Makes KYC Process Simpler: https://economictimes.indiatimes.com/news/economy/policy/rbi-makes-kyc-updation-process-simpler-no-more-re-submitting-documents-for-minor-changes/articleshow/121365608.cms