USA’s Dollar is losing monopoly.

The dollar’s reign isn’t ending, it already ended as absolute ruler. What remains is managed decline from monopoly to strong leadership. Global trade totals thirty trillion dollars annually. The dollar once controlled seventy percent of this massive market. Today it handles fifty four percent. That represents a sixteen-percentage point drop over two decades.

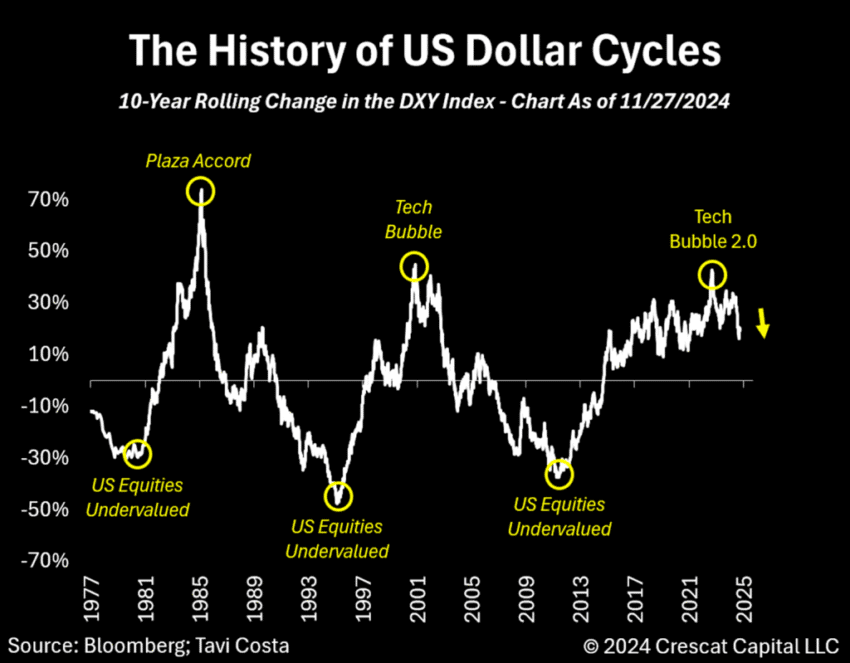

Federal Reserve data tells this story clearly. Dollar reserves peaked at seventy two percent in 2001. By 2025 they settled at fifty eight percent. This isn’t sudden collapse. It’s gradual erosion of overwhelming dominance.

Meaning of Managed Decline

Managed decline does not mean immediate collapse. It means losing absolute control while keeping essential power. Think of a king who once ruled everything now governing important territories. The dollar maintains dominance across key functions. It handles fifty eight percent of global reserves. Trade invoicing runs fifty four percent in dollars. SWIFT payment systems process forty seven percent in dollar transactions. These numbers reveal the pattern clearly. The dollar lost monopoly control but retained market leadership. Countries diversified without abandoning dollar systems entirely.

Three Pillars Standing

Network effects create the first pillar of dollar strength. Existing infrastructure and familiarity generate massive inertia. Changing currency systems requires enormous coordination costs. Liquidity provides the second pillar. Dollar markets remain the deepest and most liquid globally. When crises hit, everyone still runs to dollar assets for safety. Financial infrastructure forms the third pillar. The established ecosystem of dollar denominated instruments has no equal. Building alternatives takes decades of patient work.

Cracks Showing

Reserve diversification accelerated after 2001. Central banks added Australian dollars, Canadian dollars, euros, and yuan to portfolios. They didn’t dump dollars. They reduced complete dependence. For past few years the Central banks have been accumulating Gold.

The 2022 Russian sanctions created genuine concern worldwide. If America can freeze Russian central bank accounts, what about other countries? This planted seeds of doubt about dollar safety. Countries asked themselves a simple question. If this can happen to Russia, what about us? The fear became real. Absolute dollar dependence looked dangerous.

Alternative Systems

China pushes yuan settlements aggressively. Trade deals increasingly specify yuan invoicing. Russia built payment networks outside SWIFT. The SPFS system handles domestic transactions. India negotiated rupee trade agreements with several countries. Oil purchases from Russia happen in rupees. Other commodities follow similar patterns. Local currency deals reduce dollar dependence. These aren’t replacements for the dollar system. They’re supplements that reduce absolute dependence. Countries hedge their bets while keeping dollars for critical transactions.

Hidden Story

Foreign currency dollar credit tells the real story. 13.7 trillion dollars in credit flows to borrowers outside America. That’s five percent annual growth. This means global demand for dollar financing remains robust. But growth rates vary dramatically by region.

Asian economies show slower dollar credit growth. European markets display similar patterns. The shift isn’t dramatic yet. But direction matters more than speed. Countries that once borrowed exclusively in dollars now consider alternatives.

Trade Reality

America’s July 2025 trade deficit hit 78.3 billion dollars. The highest level in four months. This reveals structural dependence on imports despite dollar privilege. The deficit pattern shows supply chain shifts. Mexico leads at 16.6 billion. Vietnam follows at 16.1 billion. China drops to 14.7 billion. Vietnam’s emergence as major trade partner signals something important. Companies shifted production away from China. But they didn’t return to America. They found third country alternatives.

Strategic Stupidity

America weaponized the dollar system repeatedly. Iran sanctions, Russia sanctions, Venezuela sanctions. Each action taught other countries the same lesson. Dollar dependence creates vulnerability to American political whims. Smart countries reduce this vulnerability through diversification. They don’t abandon dollars immediately. They build alternatives patiently. The sanctions strategy backfired spectacularly. Instead of punishing targets, it educated everyone about dollar weaponization risks. Countries that never opposed America started building hedges.

Velocity Problem

SWIFT transaction data reveals accelerating dollar velocity. America’s share dropped to 46.94 percent of global payments. Still dominant but clearly declining. Payment velocity matters more than stock measures. Countries might hold dollar reserves but use them too quickly. This reduces demand for new dollar creation. Alternative payment systems multiply rapidly. China’s CIPS, Russia’s SPFS, India’s UPI. Europe’s INSTEX for Iran trade. Each reduces reliance on dollar clearing systems. BRICS is on edge to announce “UNIT” system soon. The network effect that protected dollar dominance now works in reverse. As alternatives gain critical mass, switching costs decrease.

Data Games

The IMF publishes sanitized data about global currency usage. Their reports emphasize dollar stability. They downplay alternative system growth. This follows a familiar pattern. Official sources hide the full picture. The Federal Reserve stopped publishing M3 money supply data in 2006. They don’t want people connecting these dots. Financial transparency threatens established power structures. Clear data would show dollar decline happening faster than admitted. Trade currency data exists for 132 countries through 2023. But it’s buried in technical reports. No clear summaries. No easy public access for independent analysis. Therefore how many smaller countries have ditched dollar is difficult to ascertain accurately.

Tipping Point

We’re witnessing monetary evolution in slow motion. The unipolar dollar system is cracking. Payment systems multiply. Currency options expand. The dollar won’t disappear overnight. But its monopoly ended already. The great managed decline has begun. America chose sanctions over cooperation. Weaponization over stability. Short term political gains over long term monetary privilege. Each choice accelerated decline. Smart empires adapt to changing conditions. They share power to maintain influence. America did the opposite. It demanded absolute submission and created resistance. The result is managed decline disguised as continued dominance. The numbers show stability. The trends show erosion. The direction is clear.

India’s Example

India embodies the alternative approach. They buy Russian oil in rupees despite American threats. They maintain strategic autonomy while avoiding confrontation. This drives American officials crazy. They imposed fifty percent tariffs on India for buying Russian oil. But India doesn’t back down. They found alternatives to dollar dependence. The Indian approach teaches other countries important lessons. You can reduce dollar dependence without declaring war on America. Strategic patience works better than direct confrontation. Other countries watch this carefully. Brazil, Saudi Arabia, Turkey, South Africa all explore similar strategies.

Debt Trap

America’s 37 trillion dollar debt creates additional vulnerabilities. Who will buy all this debt if the dollar loses reserve currency premium? Currently foreign countries buy American debt because they need dollars for trade. As trade diversifies into other currencies, this demand decreases. The math is simple but brutal. Less dollar demand means higher interest rates to attract buyers. Higher rates mean bigger debt service costs. The spiral becomes vicious. China already reduced Treasury holdings significantly. Other countries follow similar patterns. They don’t dump dollars dramatically, as it will hurt them too. They just buy fewer new ones. Existing dollars dumped for gold but slowly.

Conclusion

The dollar’s managed decline represents the end of monetary imperialism. This process started twenty years ago. Managed decline leads to shared monetary leadership. The dollar remains important but not dominant. Other currencies gain equal status gradually. It accelerates through poor American strategic choices. Countries don’t abandon dollars suddenly. They reduce dependence gradually. They build alternatives patiently. They diversify systematically. The transition to multipolar monetary systems is inevitable. Politics makes them necessary. Economics makes them profitable. America can manage this decline wisely or resist it foolishly. Management preserves significant influence. Resistance guarantees marginalization. The post dollar world isn’t anti American. It’s post American dominance. There’s a difference that smart policy can exploit. Welcome to the post monopoly world.

References:

Federal Reserve Bank of St. Louis – “The International Role of the U.S. Dollar – 2025 Edition” https://www.federalreserve.gov/econres/notes/feds-notes/the-international-role-of-the-u-s-dollar-2025-edition-20250718.html

Bureau of Economic Analysis – “U.S. International Trade in Goods and Services” https://tradingeconomics.com/united-states/balance-of-trade

Federal Reserve Bank of St. Louis – “Accessible Data: International Role of Currency vs. Size of Economy” https://www.federalreserve.gov/econres/notes/feds-notes/the-international-role-of-the-u-s-dollar-2025-edition-accessible-20250718.htm

International Monetary Fund – “Patterns of Invoicing Currency in Global Trade in a Fragmenting World Economy” https://www.imf.org/en/Publications/WP/Issues/2025/09/12/Patterns-of-Invoicing-Currency-in-Global-Trade-in-a-Fragmenting-World-Economy-570297

European Central Bank – “The International Role of the Euro” https://www.ecb.europa.eu/pub/pdf/ire/article/ecb.ireart202106_03~152e664e63.en.pdf

Society for Worldwide Interbank Financial Telecommunication – “CEO Annual Letter to Shareholders” https://www.swift.com/news-events/news/ceos-annual-letter-shareholders

Bank for International Settlements – “Global Liquidity Indicators” https://www.bis.org/statistics/gli2507.htm

Society for Worldwide Interbank Financial Telecommunication – “RMB Tracker Document Centre” https://www.swift.com/products/renminbi-tracker/document-centre

International Monetary Fund – “Data Explorer: International Trade Statistics” https://data.imf.org/en/Data-Explorer?datasetUrn=IMF.STA%3AITG(4.0.0)