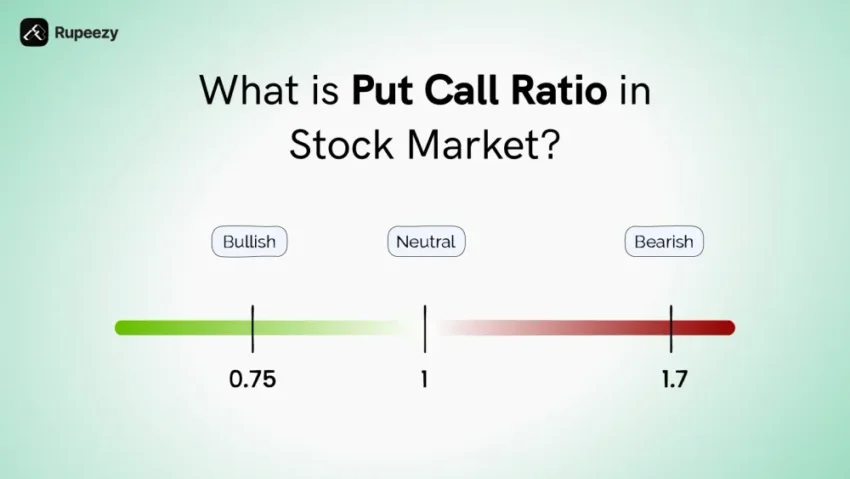

The Put-Call Dispersion Index as a Primer on Seller-Driven Risk Appetite: A Paradigmatic Reconceptualization

(Put Call Ratio Analysis)

Abstract

This paper introduces a novel interpretive framework for the Put-Call Dispersion Index (PCDI) also called Put Call Ratio (PCR), traditionally misconstrued as a mere sentiment barometer. We posit that overnight elevations in the PCDI—exemplified by a shift from 0.97 to 1.20—are not reflective of collective bearish conviction but rather indicative of amplified seller-centric premium provisioning and downside risk underwriting. Employing a discourse rich in advanced option-theoretic constructs, we demonstrate that such PCDI movements disclose the reconfiguration of latent delta exposure and gamma convexity hedging schemas, thereby reframing the index as a gauge of structural risk appetite among option writers.

Introduction

The Put-Call Dispersion Index, defined as the volumetric ratio of traded put instruments to their call counterparts, has perennially been relegated to the domain of market sentiment studies. However, prevailing expositions understate the index’s capacity to unveil the strategic calibration of risk corridors by option writers. This paper challenges orthodox sentiment-centric paradigms by reframing the PCDI as a vector of issuer-driven volatility underwriting preferences, wherein overnight escalations signal heightened appetite for tail-risk accommodation rather than latent bearishness.

Theoretical Framework

Disambiguating Sentiment from Provisioning

Conventional sentiment models treat put purchases as proxies for pessimism. Yet from a writer’s vantage, put issuance constitutes a premium accrual mechanism coupled with an intentional exposure to negative delta drift. The PCDI thus captures the premium provisioning asymmetry enacted by issuers, not the affective biases of acquirers.

Delta Exposure Realignment

An increase in the PCDI corresponds to a net augmentation of short-put deltas on the desk’s balance sheet. Issuers confronted with this delta influx implement derivative hedging routines—ranging from underlying futures acquisition to cross-gamma scalping—to preserve quasi-delta neutrality. The accelerating ratio therefore delineates a recalibration in hedging topology rather than a macroeconomic doom signal.

Gamma Convexity and Vega Harvesting

Surges in the PCDI often coincide with steepening of the implied volatility surface on the downside strikes. Writers, recognizing the embedded vega richness, may elect to vend further options or adjust strike spacings to optimize convexity carry. The observed overnight jump from 0.97 to 1.20 thus signals that sellers have identified an asymmetric vega premium opportunity and are actively consolidating it.Empirical Illustration

Consider a hypothetical equity index options book at t₀ with PCDI = 0.97. Overnight order flow propels the ratio to 1.20 at t₁. A granular audit of trade blotters reveals:

A disproportionate increase in near-the-money put issuance by principal market-making desks.

Corresponding delta-hedging buys of the underlying, aimed at neutralizing short-put exposure.

Elevations in implied volatility on the 25-delta put wing, outpacing the call side vega.

These phenomena corroborate the assertion that the PCDI uptick principally reflects seller-side risk provisioning, whereby issuers underwrite incremental downside buffers and harvest elevated volatility premia.

Discussion

Implications for Risk Calibration

Market participants, particularly institutional underwriters, should interpret PCDI ascensions as a harbinger of reinforced risk corridors on the downside. Rather than foretelling a price descent, the index alerts practitioners to the intensification of capital commitment to downside contingencies and the attendant hedging flows that may buttress price floors.

Distinguishing Provisioning from Panic

A critical analytical pitfall lies in conflating elevated PCDI readings with panic-driven protective buying. Our reconceptualization delineates two discrete regimes: the provisioning regime, wherein sellers voluntarily assume put exposures, and the panic regime, characterized by forced protective flows. Empirical diagnostics—such as skew shifts and time-decay profiles—aid in regime differentiation.

Conclusion

By inverting the canonical sentiment narrative, this paper elevates the Put-Call Dispersion Index to a diagnostic of seller-driven premium allocation and downside risk underwriting. The observed overnight shift from 0.97 to 1.20 emerges not as an omen of bearish sentiment but as a testament to fortified bullish conviction among option writers, manifested through deliberate exposure orchestration. Future research might extend this lens to cross-asset PCDI analogues and their role in systemic risk attenuation.